Wait, Why Can’t I Access All My Own Money?

Yep, that’s often the first thought.

You’re running a business, sales are coming in, everything seems smooth—until you realize your payment processor is withholding a portion of your funds.

Not permanently. But… still. They say it’s for protection. You call it frustrating.

Let’s talk about what this really is.

It’s called a rolling reserve, and if you’re operating a high-risk merchant account, chances are you’ve already met it or will soon.

But no, it’s not a punishment. And once you understand how it works, you might even see why it’s there.

Let’s break it down. Real talk.

So, What Is a Rolling Reserve?

In simplest terms?

A rolling reserve is a small portion of your daily or weekly credit card sales that your payment processor holds onto for a certain time, usually between 90 to 180 days.

You can think of it like a safety net your provider keeps, just in case there are chargebacks, fraud issues, or surprise refunds down the road.

Let’s say you’re in one of the top 10 high-risk industries, maybe you sell supplements, run a subscription box, or manage a travel platform. These verticals are more prone to disputes and refund requests.

So, the processor holds on to a slice of your earnings temporarily. Once the reserve window ends, you start receiving those withheld funds on a rolling basis.

It’s a little like saving money for a rainy day, except your provider is doing it on your behalf.

Why Do High-Risk Accounts Get Hit With This?

Because volatility freaks out banks.

And risk—whether from high chargeback ratios, long delivery cycles, or compliance issues—makes everyone nervous.

If you’ve ever read up on high-risk vs low-risk merchant accounts, you’ll know this already: high-risk merchants walk a tighter rope. Providers need to protect themselves. And you. Even if it doesn’t always feel that way.

So yeah, this is standard protocol if you’re in a high-risk business.

Pro Tip: Getting your business structure and documentation right from day one really matters. If you’re still operating without proper compliance or formation, you’re already flagged. Many of our clients found a smoother path after forming their company the right way, with guidance that checks all the compliance boxes upfront.

How Much Do They Hold and for How Long?

Here’s the thing: there’s no one-size-fits-all answer.

It depends on your provider, your history, and your business model.

Most of the time, rolling reserves take around 5% to 10% of your daily credit card sales, and they’re usually held for 60, 90, or even up to 180 days.

Some providers adjust this over time, so if your dispute ratio drops or your monthly volume grows steadily, the reserve terms might ease.

If you’re still figuring out how to choose the right high-risk merchant provider, make sure to ask:

- “What’s your reserve policy?”

- “Can this be negotiated later?”

- “Is it rolling or fixed?”

Transparency matters more than anything else here.

Oh, and by the way, this isn’t the only way reserves are handled. Let’s quickly clear up one common confusion…

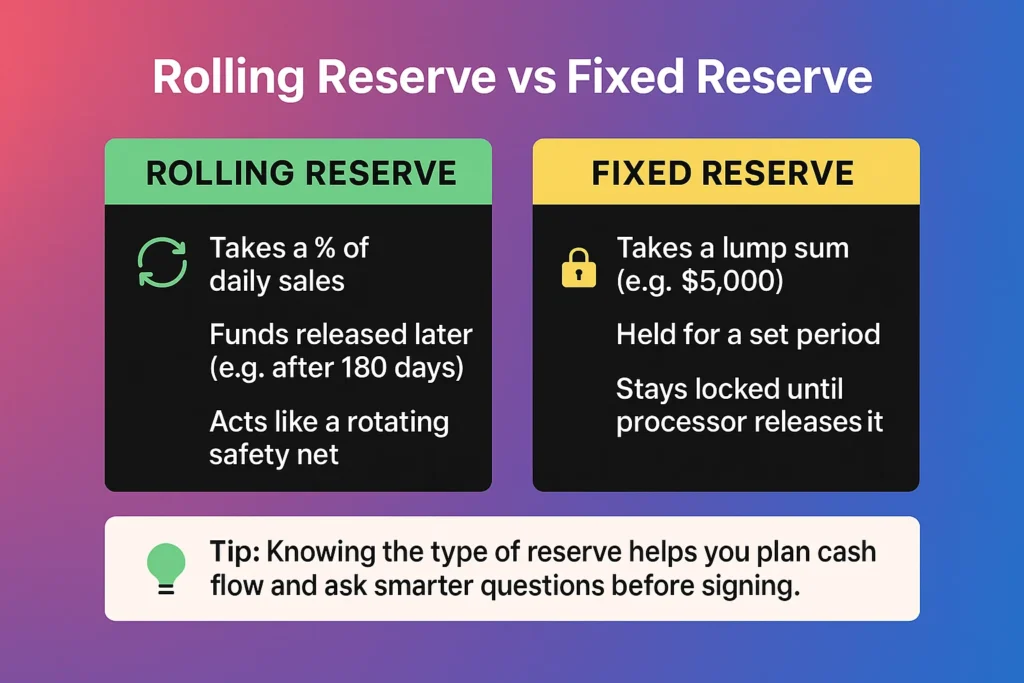

Rolling Reserve vs. Fixed Reserve: Know the Difference

A quick heads-up: not all reserves roll.

- Rolling reserves take a percentage of your daily sales and return them on a timed cycle (like 180 days later). Think of it as a constantly rotating safety net.

- Fixed reserves, on the other hand, take a lump sum—say, $5,000—and lock it up for a set period. It doesn’t “roll.” It just sits there until your processor feels safe enough to release it.

Knowing which one you’re dealing with can help you plan cash flow better and ask smarter questions before signing any merchant agreement.

Can You Avoid Rolling Reserves Altogether?

Honestly? Sometimes, but rarely.

Unless your provider is willing to take a bigger risk on your behalf (which usually means higher fees somewhere else), a rolling reserve is pretty much baked into the deal.

What you can do, though, is:

- Negotiate the rate based on your industry averages.

- Improve the processing history to revisit the terms later.

- Reduce chargebacks proactively—yep, remember that one? (If not, now’s a good time to brush up on strategies to reduce chargebacks.)

Bottom line: the better your business behaves, the more leverage you have.

What If It’s Hitting Your Cash Flow?

This is where it gets real.

Cash flow can be the difference between scaling or stalling—especially in fast-moving sectors. And having 10% of your income delayed for months?

That hurts.

So here’s a tip: plan for it upfront. Build your budget knowing there’s a buffer. Treat that reserve like untouchable savings. If you rely on it to meet everyday costs, you’ll constantly feel squeezed.

Also, don’t forget: different providers have different policies. If one’s hurting your growth, explore your options. (Not all High-Risk Merchant Services are built equally.)

The Smarter Way to View It

Think of the rolling reserve as financial armor, not handcuffs. Yes, it feels restrictive. But it’s also the reason your provider is willing to take a chance on you in the first place.

And if you’ve made peace with the other quirks of this space, like risk flags, verification loops, or the eternal debate of what high-risk merchant services are anyway, then this, too, is part of the package.

Just know what to expect, and don’t let it catch you off guard.

Let’s Wrap It Up

Running a high-risk business is already tough enough. So don’t let a rolling reserve become a mystery or a monster. That’s just how the game works.

The more you understand it, the better you can negotiate, plan, and pivot—without losing sleep over “missing” money.

“Not all restrictions are walls; some are safety nets. Know which one you’re standing on.”

FAQ

Why is my provider keeping a portion of my sales? Isn’t that my money?

Answer: Yep, it is your money. But in the high-risk world, payment processors hold a slice as a security buffer in case of disputes or refunds. It’s not permanent. It’s just their way of saying, “Let’s be cautious, just in case something goes sideways.” That chunk is called a rolling reserve, and it eventually rolls back to you.

How long does a rolling reserve last in high-risk merchant accounts?

Answer: Usually? Anywhere from 90 to 180 days. But don’t panic, it’s not a lump sum held forever. Think of it like a moving window. Funds from Day 1 get released on Day 91, Day 2 on Day 92… and so on. If you manage disputes well and keep your High-Risk Merchant Account clean, some providers may shorten the hold period.

Can I negotiate my rolling reserve terms?

Answer: Absolutely. Not always upfront, but over time? For sure. If you show consistent transaction volume, low chargebacks, and reliable processing behavior, many providers will revisit your terms. It helps to ask the right questions early, especially when choosing the right high-risk merchant provider.

What if the rolling reserve is killing my cash flow?

Answer: Then it’s time to regroup. Either plan tighter cash cycles, renegotiate terms, or explore providers with more flexible policies. Some businesses even consider merchant cash advance services or short-term funding to bridge that reserve gap, though that comes with its own risks. Bottom line: know your limits, and build your operations around the reserve, not against it.

Do all high-risk businesses face rolling reserves?

Answer: Not always, but most do. Especially if you’re in industries like supplements, adult, travel, crypto, or coaching, aka the usual suspects in the top 10 high-risk industries. Even within low-risk industries, if you’ve got a poor history or high disputes, your account might still get flagged for a reserve.

How can I ease the strain of a rolling reserve on my business?

Answer: Three words: Reduce.Your. Chargebacks. That’s your best card to play. Improve your customer service, set realistic expectations, and always deliver on time. Knowing how to reduce chargebacks isn’t just about avoiding fees; it can improve your entire risk profile, including those reserve terms.